Mid-Year Survey: Colorado Businesses Stay Growth-Minded As They Manage Tariffs, Trade Uncertainty (Photo) -07/22/25

More than 6 in 10 prioritize investments over cost-cutting; focus on tools to enhance efficiency

Umpqua Bank recently conducted a mid-year survey of small and midsized businesses across Colorado on their 12-month economic outlook, growth plans, and response to tariffs, generative AI and cybersecurity.

While general optimism and plans for growth are somewhat muted by the need to navigate economic uncertainty and potential tariff impacts, decision-makers are relatively confident in their prospects for continued success. Compared with businesses operating in other parts of the country, they are growth-focused and leading in generative AI adoption, while prioritizing investments that create efficiency and protect working capital.

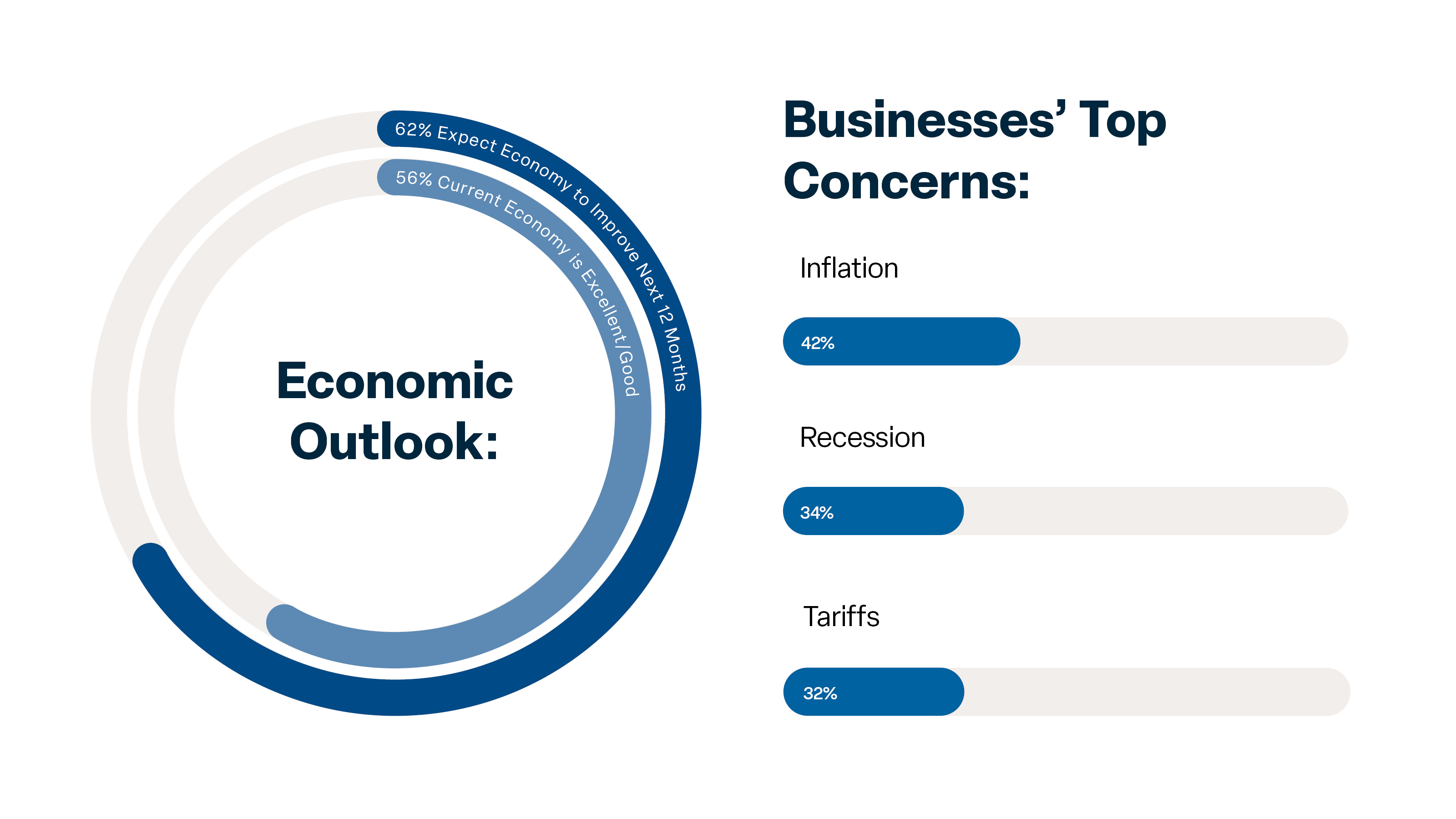

Outlook & Top Concerns

A majority (56%) of businesses surveyed rate the current economy as excellent or good; 62% also expect the economy to improve over the next 12 months—up from 52% in 2024, and much stronger than this year’s national average (47%).

Consistent with other parts of the country, inflation ranked as a top three concern for 42% of respondents, followed by possible recession (34%) and tariffs (32%).

Adjusting to Tariffs, Trade Uncertainty

Many companies have already taken measured steps to manage potential tariff impacts. Rather than making wholesale changes to foreign operations or supply chains, businesses have been planning for a range of modest actions, including price adjustments, negotiating costs with suppliers, looking for additional sources both domestically and internationally, and accelerating sales timelines, among other strategies.

For those with facilities or sourcing operations abroad, the prospect of tariffs is having limited impact on near-term decisions to reshore operations or source materials domestically. In fact, nearly 7 in 10 leaders surveyed still plan to maintain or increase their current levels of foreign trade activity and exposure over the next 12 months.

Balancing Growth Expectations and Financial Challenges

Colorado businesses continue to balance relative optimism and expectations for growth with managing financial concerns.

They are upbeat about business prospects over the next 12 months, with those surveyed much more likely to prioritize making investments than cost-cutting. Many expect increases in revenue (55%), demand for products and services (49%), profitability (38%), and the number of employees (33%). Growing the business, especially revenues, is most cited as the key to success.

Investment priorities reflect the balance between growth opportunities and financial management. Top priorities include investing in digitization to improve efficiency (95%),

protecting payment systems (81%), making significant changes to products or services (74%), accessing capital to finance expansion (55%), and expanding their real estate footprint (46%).

“Decision-makers are countering any potential price and cost increases with productivity gains, as they focus investment on tools that enhance efficiency,” says Shawn Thompson, Umpqua Bank’s Middle Market Regional Director, Mountain & Southwest. “They also signal a willingness to re-imagine products and services to stay relevant and ahead of the competition.”

Leading on AI and Cybersecurity

AI remains a top investment priority for Colorado businesses, with 85% likely to invest or expand AI tools over the next 12 months. They’ve made significant progress implementing AI technology, and a strong majority feel confident in their pace of adoption compared to peers (71%). Half also report that, at least right now, AI implementation has actually led to increased staff levels, compared to 6% reporting a decrease. Leaders cite AI’s positive impact on improved decision-making, productivity and profitability as fueling the increase.

Cybersecurity and related fraud are also top of mind, and businesses are taking steps to combat related threats. In the last 12 months, most have prioritized cybersecurity and anti-fraud enhancements by using bank fraud prevention solutions (74%), emphasizing employee training (74%), tightening internal controls (70%), and conducting regular audits to identify vulnerabilities (58%). While 91% feel at least moderately well prepared to prevent an attack, less than 4 in 10 feel very well prepared.

“With cybersecurity and fraud, preparation is key,” says Kathryn Albright, Umpqua Bank’s Head of Global Payments and Deposits. “Regularly train employees on the latest schemes. Look at your internal controls, conduct regular audits to identify vulnerabilities and use bank fraud prevention solutions. Leaders in this space will not only guard against financial losses but also give themselves another competitive advantage.”

To download Umpqua Bank’s 2025 Business Barometer report on U.S. small and midsize businesses, visit umpquabank.com/

Umpqua Bank is a leading regional financial institution supporting businesses of all sizes and consumers across the western U.S. With more than $50 billion in assets, Umpqua is the third largest publicly traded bank headquartered on the West Coast.